Agentic Payments-Next Frontier in Fintech

How autonomous AI agents are creating the biggest payment revolution since digital wallets

This is the first article in a three-part series unpacking Agentic Payments, the new fintech buzzword.

Let’s start with an example.

Imagine this: Your AI agent sees that a major industry conference you want to attend just opened early-bird registration on your e-mail. It scans your calendar, confirms there are no conflicts, checks flight and hotel prices, applies loyalty points, and books the entire trip: flights, hotel, transport, and conference pass, all within your budget. You receive a single, concise itinerary. No forms, no back-and-forth emails, no approval bottlenecks. Just one autonomous execution. Fascinating isn’t it?

This is example of how Agentic Payments might work. This isn't science fiction, and it's about to transform how money moves without human involvement. But we are not there yet.

TechCrunch evaluation of Perplexity’s1 shopping agent revealed what should be instantaneous purchases took between 3-8 hours to process, with frequent transaction failures. When trying to buy simple items like toothpaste, orders were canceled after hours of waiting because items were "sold out", despite being available on the retailer's website.

There is a fundamental mismatch between our expectations for Agentic Payments-hyped use cases and how much the current payments infrastructure can support. In this article, I will outline how Agentic Payments are different, the market opportunity as well the gaps in current infrastructure to support Agentic Payments

“Welcome to the age of Agentic Payments”

What makes Agentic Payments different?

Every prior payment innovation from credit cards to PayPal to mobile wallets aimed reduced friction for human users. Credit cards eliminated the need to carry cash. PayPal made online payments safer. Mobile wallets made checkout faster. These were incremental improvements to what was fundamentally a human process.

Agentic payments break that pattern entirely. Instead of making it easier for humans to pay, they remove humans from payment loops entirely.

Autonomy: AI agents don't just execute payments, they can monitor usage patterns, compare alternatives across vendors, negotiate terms, and switch services as well, without any human intervention.

High speed: Agents can initiate and complete thousands of transactions per second, operating at frequencies impossible for human-mediated systems.

Real-time context: AI understands intent, processes context, and optimizes decisions in milliseconds, adapting to changing conditions without pre-programmed rules.

Market opportunity:

Agentic Payments industry is being built on the backbone of two massive sectors:

Digital Payments, expected to reach $36.75 trillion globally2 and

AI Agents, a market set to grow to $216.8 billion by 20293

While it’s unlikely that agents will take over every transaction, conservative adoption estimates suggest that 1 to 4 percent of all digital payments could be handled autonomously within the next five years.

Why did I choose a below 5% adoption rate for Agentic Payments?

Historically, payment innovations like contactless payments and mobile wallets took over a decade and half to reach 10-25% market penetration despite being incremental improvements to existing systems4, Agentic Payments face even steeper adoption challenges as fundamental changes to infrastructure, compliance frameworks, and legal accountability structures is required for their adoption.

The number might seem small in percentage terms, but the math tells a different story:

From the graph above, at 1-4 % rate of penetration, the transactions valued between $367.5 billion-$1.47 trillion would be made by AI Agents by 2029.

Let’s get into a little more detail:

Some types of payments, especially in the B2B space are more suited for automation. Transactions that are predictable, repetitive, and follow clear rules are easier for agents to manage without human oversight. In contrast to complex, once-in-a-while heavy transactions that still require manual review, more routine payments can be performed by agents that monitor systems and trigger actions based on a predefined logic.

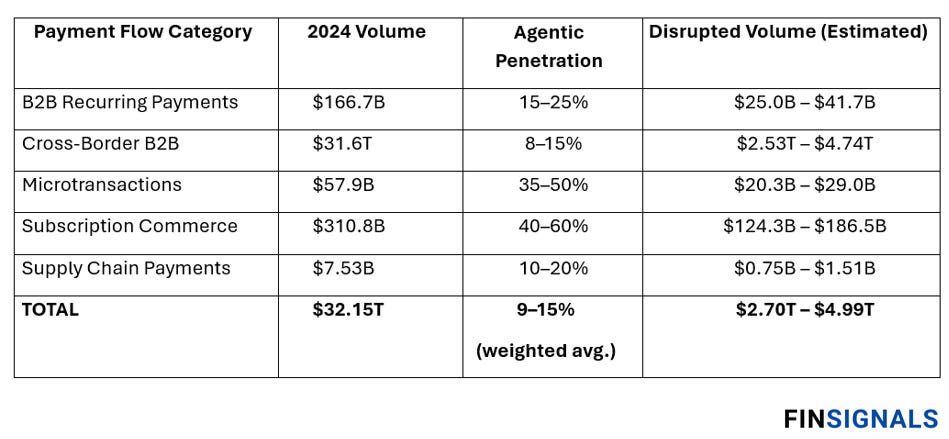

Based on this reasoning and my hypothesis, I’ve identified five payment categories that are likely to see earlier adoption and offer strong ROI potential for Agentic Payments. These categories reflect transaction types that are already structured and routine.

In the table below, I’ve estimated the potential volume of disrupted payments by applying an estimated agentic penetration rates to each category.

(Brainstormed these numbers and rationale with Claude)

Agentic payment adoption is expected to be moderate for B2B recurring payments (15–25%) and supply chain payments (10–20%) due to early-stage infrastructure and complex workflows.

Cross-border B2B payments will see lower penetration (8–15%) because of regulatory and compliance hurdles.

In contrast, microtransactions (35–50%) and subscription commerce (40–60%) are likely to see higher agentic adoption, since automation delivers the most value in high-volume, low-value or recurring payment scenarios, and streamlines customer experience and billing.

But can the current infrastructure keep up?

The entire payments ecosystem was architected for humans, not machines. Every payment layer from banks to card networks to merchant systems contains friction designed to prevent exactly what AI agents need to do: make rapid, autonomous transactions.

1. Human-centric design:

Current systems are built on the assumption that a human is initiating and approving each transaction. As a result, these systems introduce friction through authentication, manual checks, transaction limits, and delays to prevent fraud. These controls, though necessary for human use, become obstacles for AI agents that need to act quickly, independently, and at scale.

While tokenization solutions like Mastercard's Agent Pay are emerging to address authentication challenges, there is a fundamental architectural mismatch between human-designed systems and machine-driven transactions.

2. Identity and compliance frameworks lack digital-native standards:

AI agents don't have biometrics, passports, or government IDs. KYC (Know Your Customer) and AML (Anti-Money Laundering). Regulations demand these human identifiers before anyone can access the financial system. Banks globally paid $26 billion in fines5 in recent years due to non-compliance with AML, KYC, and sanctions rules, often because outdated systems cannot meet modern compliance demands. These compliance frameworks were built for human onboarding and already face challenges in that context, making them even less suited for AI agents operating autonomously at scale.

The challenge extends beyond mere identification.

How do you verify that an agent is acting on behalf of a real, authorized individual?

Our infrastructure has no universal standard for assigning, verifying, or revoking agent permissions.

Regulators do not yet have clear frameworks for assigning legal responsibility or ownership for. This makes large-scale adoption of agentic payments difficult to manage and creates significant compliance risks for financial institutions.

The entire compliance stack is built around human initiation and responsibility. AI agents, however, operate autonomously and often across jurisdictions, time zones, and markets.

3. Legacy payment rails cannot handle machine-speed commerce

Despite the impressive headline capacity of legacy payment networks like Visa, which can process up to 65,000 transactions per second (TPS)6 and the rapid growth of real-time alternatives such as India’s UPI (averaging 3,729 TPS)7, the global payment infrastructure remains fundamentally designed for human-scale commerce.

Settlement systems like ACH and SWIFT still rely on batch processing, with ACH transactions typically clearing in one to two business days and SWIFT payments taking one to four business days, creating significant latency for time-sensitive, high-frequency agentic transactions. Even newer “instant” payment solutions like FedNow have seen adoption surge, but their throughput and network coverage are nascent, and limiting their utility for continuous, high-volume agentic commerce. As a result, today’s payment rails cannot efficiently support the scale or speed at which AI agents operate.

4. Fraud detection systems

Modern fraud detection systems use machine learning to spot patterns and behaviors linked to potential fraud, helping strengthen defenses against financial crime. But these same systems often become roadblocks for legitimate AI agents.

Global losses from transaction scams are expected to reach $206 billion by 2025, up from $130 billion in 2020, driving financial institutions to implement increasingly sophisticated detection mechanisms8. The challenge is that many characteristics of effective AI agents such as high transaction velocity, unusual spending patterns, cross-platform activity mirror fraud behavior.

Current systems offer 24/7 fraud detection with machine learning models trained on historical data, but they lack the context to distinguish between malicious bots and beneficial AI agents.

This creates a fundamental tension: the more sophisticated and autonomous an AI agent becomes, the more likely it is to trigger fraud prevention measures.

5. Absence of Universal Governance and Standards

The lack of standardized governance frameworks presents perhaps the most critical barrier to widespread agentic payment adoption.

Currently, there's no universal protocol for establishing, communicating, or enforcing an AI agent's transaction boundaries across different financial systems. When an agent attempts to make a purchase, merchants, banks, and payment processors have no standardized way to verify its authorization scope, spending limits, or operational constraints. This creates a fragmented ecosystem where each platform develops proprietary solutions—Google, Visa, Mastercard, and PayPal are all building their own agentic commerce infrastructures, but these operate as isolated silos rather than components of an interoperable network.

Without industry-wide standards for agent identity verification, permission management, audit trails, and cross-platform policy enforcement, the ecosystem remains vulnerable to misuse and fraud.

In conclusion, Agentic payment rails would need to support entirely different requirements: nanosecond authorization, dynamic spending parameters that adjust based on market conditions etc. This infrastructure would require standardized agent authentication protocols, real-time cross-platform permissions, and automated verification—creating a unified foundation where any AI agent, regardless of its origin platform, could transact seamlessly with any merchant or service provider while maintaining security, accountability, and regulatory compliance at machine scale.

I hope this gave you a starting point in the agentic payments space. In the next article, I’ll dive into how the current ecosystem is adapting and how incumbents are shifting their strategies to keep up.

https://techcrunch.com/2024/12/02/the-race-is-on-to-make-ai-agents-do-your-online-shopping-for-you/

https://electroiq.com/stats/online-payment-statistics/

https://www.businesswire.com/news/home/20250508203358/en/AI-Agents-Market-Industry-Trends-and-Global-Forecasts-to-2035-AI-Agents-Market-Set-to-Skyrocket-from-USD-5.29-Billion-to-USD-216.8-Billion-by-2035---ResearchAndMarkets.com

https://www.pymnts.com/wp-content/uploads/2022/07/PYMNTS-Mobile-Wallet-Adoption-August-2022.pdf

https://resources.fenergo.com/newsroom/global-financial-institutions-fined-26-billion-for-aml-sanctions-kyc-non-compliance

https://www.bitget.site/wiki/how-many-transactions-per-second-visa

https://timesofindia.indiatimes.com/technology/tech-news/upi-surpasses-worlds-leading-digital-payments-platforms-with-this-record/articleshow/112949499.cms

https://www.paymentsdive.com/news/payments-fraud-losses-prevention-nilson-outlook/737440/